June 19, 2026

How to Stop Relying on Cash Advance Apps

A practical plan to treat cash advance apps as a bridge, not a habit, and shrink the advance you need each payday to zero.

Read article

Somewhere along the way, someone told you that you need three to six months of expenses saved, did the math, realized it was thousands of dollars you do not have, and decided the whole thing was hopeless. So you saved nothing. I get it, and I want to gently take that number off the table, because it is the reason a lot of people never start.

You do not need six months saved. Your first goal is much smaller and much more reachable: a $500 starter buffer. That is enough to absorb the emergencies that actually happen to most people, and building it on a low income is not about having incredible discipline. It is about starting absurdly small and making the saving automatic. Here is how.

The nonprofit America Saves, part of the Consumer Federation of America, recommends starting with a $500 emergency fund, and I think that target is exactly right for a reason most advice misses. Five hundred dollars is not arbitrary. It is roughly what the common, real-life emergencies cost: a car repair, a medical co-pay, a replacement tire, a broken appliance. Those are the surprises that quietly push people into high-cost debt. A $500 cushion stops most of them from becoming a payday loan or an overdraft spiral.

America Saves also cites a striking finding: research suggests low-income families with at least $500 saved were better off financially than moderate-income families with less than that set aside. Read that again if you need to. Having a small buffer mattered more than earning more. The dollar amount you can reach is more powerful than the salary you cannot control right now.

A starter buffer does something out of proportion to its size: it keeps a surprise from turning into a debt you carry for months. Without a cushion, a $300 car repair goes on a credit card or an advance, and you pay interest or fees on it for a long time. With a cushion, it is annoying and then it is over.

The research on this is encouraging. The CFPB found that people who save even a little for emergencies tend to have higher credit scores and are less likely to fall behind on bills or turn to payday and title loans. That study is from 2022, but the behavioral pattern holds up. And you are far from alone in starting from zero: Bankrate found that 27% of Americans have no emergency savings at all, and 59% could not cover a $1,000 emergency from savings. You are not behind some crowd of savers. You are with the majority, and a small buffer moves you out of it.

The single most effective tactic, the one that matters more than any other, is to make saving automatic so it happens before you can spend the money. On a low income, waiting until the end of the month to save what is left does not work, because there is never anything left. So flip the order. Pay the buffer first.

Once it is automatic, saving stops depending on how disciplined you feel on a hard Friday. The transfer just happens, quietly, and the buffer grows while you are busy living your life.

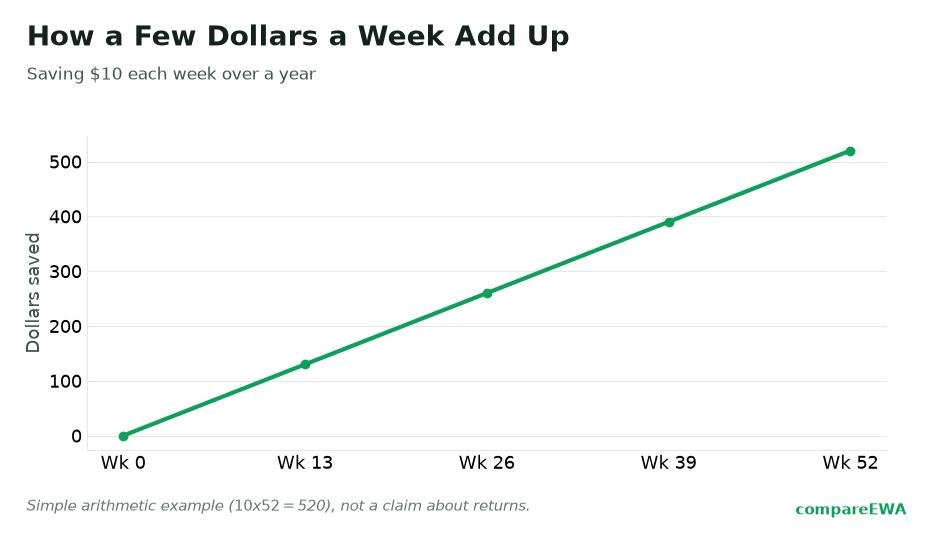

Small is not a consolation prize here. Small is the strategy. A $5 or $10 weekly transfer is completely legitimate, and early on the habit matters far more than the amount. Let me show you what a gentle ladder to $500 can look like.

Roughly a year, mostly on $5 and $10 weeks, gets you to a buffer that changes how surprises feel. And some weeks there will be nothing to spare. That is real life, not failure. Skip that week and resume the next. The ladder bends; it does not break.

You want the buffer close enough to reach in a true emergency, but far enough away that you do not accidentally spend it on a Tuesday. The sweet spot is a separate savings account, ideally at a different bank or credit union from your checking, so moving money to it takes a deliberate step. A high-yield savings account is a fine option if you have access to one, though the rates change over time, so do not chase yield. The main job of this account is not to earn interest. It is to be there, liquid, when the tire blows.

The weekly transfer is your engine, but you can jump the buffer forward with money that was never in your everyday budget to begin with. This is where a low income can still build a cushion surprisingly fast.

Because this money never felt like "yours" to spend, it is the easiest to save without the pinch.

A buffer only works if you protect it, so decide now, while you are calm, what qualifies as a real emergency. My simple test: it has to be true, urgent, and unexpected. All three.

A car repair you need to get to work is an emergency. A surprise medical co-pay is an emergency. A concert ticket, a sale that ends Sunday, or a bill you knew was coming is not, even when it feels pressing in the moment. Writing the definition down ahead of time keeps you from talking yourself into draining the fund for something that could wait. The buffer is not spending money you have not touched yet. It is protection you are keeping loaded.

There is a stretch, early on, where an emergency could hit before your buffer is ready. That is the honest gap in every "just save $500" plan. During that window, an earned wage access advance can bridge a genuine shortfall without pushing you into a payday loan. Use it carefully: take the free transfer, set any tip to $0, and remember it shrinks your next paycheck. And keep it in perspective. The advance is a temporary patch. The buffer is the thing that ends the reliance on advances, because once you have a few hundred dollars set aside, you cover the emergency yourself and keep the fee.

Let me put it together for someone on a genuinely tight budget. Say you take home about $2,200 a month and your margin is thin.

Six to seven months, built almost entirely on $10 Fridays plus two chunks of money that were never in your monthly budget. Then a $250 car repair shows up, and instead of an advance or a credit card, you pay it from the buffer, refill it over the next couple of months, and never touch high-cost debt. That is the whole point of the $500. Not wealth, just a floor under your feet.

Aim for a $500 starter buffer, not the traditional three to six months of expenses. Five hundred dollars covers the most common real emergencies, like a car repair or a medical co-pay, which are the surprises that usually push people into high-cost debt. Once you reach $500, you can build toward larger goals, but $500 is the target that actually stops most crises.

Automate a small transfer on payday before you spend, even $5 or $10, and send it to a separate account. Waiting to save whatever is left over does not work on a tight budget, because there is rarely anything left. Making it automatic means the saving happens first, and you can fund it faster with money you did not plan on, like a tax refund or an extra shift.

As a starter, yes. Five hundred dollars covers most common emergencies and keeps a surprise from becoming debt. Research cited by America Saves even found that low-income families with $500 saved were better off financially than moderate-income families with less. It is not your final goal, but it is the milestone that changes how emergencies feel, and it is reachable on a low income.

In a separate savings account, ideally at a different bank or credit union from your checking, so it is close enough to reach in a real emergency but not so handy that you spend it by accident. A high-yield savings account works if you have access, but do not chase interest rates. The main job of this account is to be liquid and available when you need it.

Something that is true, urgent, and unexpected, all three at once. A car repair you need to get to work or a surprise medical co-pay qualifies. A sale, a concert, or a bill you already knew was coming does not, even if it feels pressing. Deciding the definition in advance, while you are calm, keeps you from draining the buffer for non-emergencies.

A common approach is to build a small starter buffer of around $500 first, then focus on debt, then return to grow the fund. Without any cushion, the next surprise just puts you right back into new debt, undoing your payoff progress. The small buffer breaks that loop. Keep making minimum payments on your debts while you build it.

A practical plan to treat cash advance apps as a bridge, not a habit, and shrink the advance you need each payday to zero.

Read article

Small, doable moves to make your paycheck last through the long last week before payday, built on realistic numbers.

Read article

A step-by-step, shame-free plan to stop living paycheck to paycheck and build a little breathing room between deposits.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking