May 21, 2026

New York Earned Wage Access Law: The Rules Now

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

If you live in California and you've thought about tapping an app to grab part of your paycheck a few days early, there's a specific set of rules sitting behind that button now. The California earned wage access law took effect on February 15, 2025, and it changed who is allowed to offer these advances to California residents and what those companies have to promise you in return. It did not, however, cap what they can charge. That gap matters, and I'll get to it.

Here's the short version before the detail: these apps are legal in California, they now answer to a state regulator, and the protections you get come mostly from a registration system rather than a price limit. Let's walk through what that actually means for the person holding the phone.

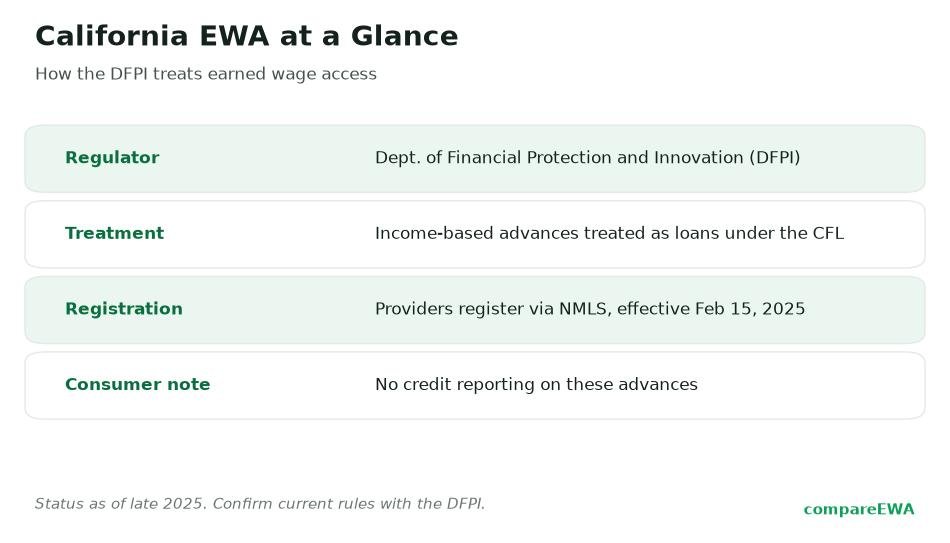

Yes. Earned wage access apps, which California officially calls "income-based advances," are legal in the state. As of February 15, 2025, though, there's a condition attached: only a company that has registered with the state, applied to register, or qualifies for an exemption may offer these advances to California residents. That rule comes from the California Department of Financial Protection and Innovation, the DFPI.

So the product is permitted, but the provider behind it is supposed to be on the state's radar. If an app is operating in California and hasn't registered or applied, it's out of step with the rule. That's a meaningful shift from the free-for-all that existed before, when any provider could market to Californians with no state oversight at all.

The DFPI is California's financial watchdog. It supervises a long list of financial products and companies under two main authorities: the California Consumer Financial Protection Law (the CCFPL) and the California Financing Law (the CFL). Think of it as the state's version of a consumer-finance cop, with the power to write rules, take registrations, and act against companies that break them.

For earned wage access specifically, the DFPI spent nearly two years building the current framework, and the path was not smooth. The agency first proposed treating income-based advances as loans under the CFL back in March 2023. California's Office of Administrative Law (OAL), the body that reviews state regulations for procedural soundness, disapproved that first attempt on April 26, 2024, citing problems with how it complied with the Administrative Procedure Act. The DFPI reworked it. The OAL signed off on the revised registration rulemaking on October 11, 2024, and the rules went live the following February.

Why does that backstory matter to you? Because a lot of older articles were written during the messy middle, when the rules were only proposed or had just been rejected. The framework you're living under now is the finished one, and it looks different from those earlier drafts.

The heart of the California earned wage access law is a registration regime run through the Nationwide Multistate Licensing System and Registry, the same NMLS platform that handles many other financial licenses across the country. A provider that wants to serve Californians registers there, pays an initial application fee of $350 and a $100 annual renewal, and takes on ongoing reporting and conduct obligations.

The rule also draws a tight box around what counts as an "income-based advance." To fit the definition, an advance has to be:

That last piece is the part I'd underline. A registered California provider promises, as a condition of the definition, not to send your unpaid advance to collections, not to sell that debt, and not to ding your credit report over it. That's a real, concrete protection, and it's baked into what the product legally is.

You may have read that California treats these advances as loans. That's accurate, but it's easy to misread. The rules do classify income-based advances as "loans" for the purposes of the California Financing Law's definitions. In plain terms, the state uses its lending statute as the legal home for the product.

What that classification does not mean is that you're taking out a payday loan or that the full weight of California's lending-license rules lands on the provider. The DFPI deliberately built a lighter path: instead of forcing these companies through the entire CFL licensing regime, it lets them register under the CCFPL and follow the conduct and reporting duties that come with registration. So "it's a loan" is a definitional label with limited practical bite. It's the hook the state used to claim authority, not a signal that you're borrowing at payday-loan terms.

This is exactly the kind of distinction worth keeping straight. An advance you repay from your own next paycheck, with a promise of no collections and no credit reporting, behaves very differently from a storefront payday loan even when both sit under the same statutory roof. If you want the fuller side-by-side, our breakdown of earned wage access versus payday loans gets into the cost math.

Let me separate what the law gives you from what it leaves open, because both are real.

What you get: a provider that has to be registered (or applying, or exempt) to serve you, a non-recourse promise so an unpaid advance can't be sold or sent to collections, no credit-bureau reporting on that advance, and a company that now files reports with a state regulator that can act if it misbehaves. If something goes wrong, you have a place to complain, and the DFPI has authority to respond.

What you don't get: a cap on what the app can charge you. The final rule does not require an APR-style disclosure, and it doesn't set a hard ceiling on fees. Your protection runs through registration and the non-recourse warranty, not through a price limit. That's the honest picture, and it's why linking your bank account still calls for a careful read of the fee screen. Before you connect any app, it's worth understanding what these apps can see once you link your bank.

Earlier drafts of the DFPI's rules floated fee caps. The final version dropped them. Instead, the regulation defines the kinds of "charges" a provider may collect, and the list is broad: subscription fees, expedited-funds fees (the charge to get your money instantly instead of waiting), account-transfer fees, gratuities (the "tips" many apps request), and other optional or discretionary payments.

So California tells providers which categories of charges are allowed, but it doesn't say how high any of them can go. For you, that means two apps operating legally in the state can charge very different amounts for the same $100 advance, and neither is breaking the rule. The instant-transfer fee and the tip prompt are where the real cost usually hides. Don't assume "regulated" means "cheap." It doesn't, at least not here.

This is also where a comparison helps more than a single app's marketing. Looking at fee structures side by side is the whole reason our EWA app rankings exist, and our review of the top-rated option, Cashzella, lays out its costs in one place.

Here's the twist that makes California's approach more important, not less. While California was building state oversight, the federal government moved in the opposite direction. On December 23, 2025, the Consumer Financial Protection Bureau reaffirmed that qualifying earned wage access is not "credit" under the federal Truth in Lending Act, and it rescinded a July 2024 proposal that would have treated many of these products as credit. You can read the action in the Federal Register notice on the non-application of Regulation Z to EWA products.

Translated: the main federal consumer-lending disclosures, the ones that would spell out an advance's cost in standardized terms, generally don't attach to qualifying EWA. That pushes the job of protecting you down to the states. In a state with no EWA rules, that leaves a thin safety net. In California, at least you have registration and the non-recourse warranty, even without a fee cap.

California isn't alone in stepping up as the federal role recedes. A handful of states have written their own EWA laws, and they don't all look alike. Nevada, for instance, went further on consumer protections, as our piece on the Nevada earned wage access law explains. You can read the DFPI's own materials on income-based advances at the Department of Financial Protection and Innovation, which is the binding authority here (law-firm summaries are useful corroboration, not the rule itself). And if you want to confirm whether a specific provider is registered in California, the NMLS Consumer Access site lets you look companies up directly.

One practical caution: registration lists change. Before you trust an app in California, check that its provider actually shows up as registered or applying, rather than taking the app's word for it. The rule only protects you if the company is inside the system.

Yes. Earned wage access apps, which California calls income-based advances, are legal. Since February 15, 2025, only providers that are registered with the DFPI, have applied to register, or qualify for an exemption may offer them to California residents.

It does. The California Department of Financial Protection and Innovation oversees income-based advance providers under the California Consumer Financial Protection Law, using a registration system run through the NMLS. Providers take on reporting and conduct obligations once registered.

For definitional purposes under the California Financing Law, yes, the rules label income-based advances as loans. But that classification is narrow. Registered providers follow a lighter CCFPL registration path rather than the full lending-license regime, so it does not mean you are taking out a payday-style loan.

Registered providers must warrant that they will not send an unpaid advance to collections, will not sell or transfer the debt, and will not report it to a credit bureau. Users also gain a state regulator, the DFPI, that can act against providers that break the rules.

No. The final DFPI rule dropped earlier proposed fee caps and does not set a hard ceiling on charges. It defines which charges are allowed, including subscription fees, expedited-funds fees, transfer fees, and tips, but not how high they can go. Compare fees carefully before signing up.

That is the date the DFPI's registration rules took effect. After it, only registrants, applicants, or exempt entities may lawfully offer income-based advances to Californians, and those providers carry the non-recourse and no-credit-reporting warranties built into the rule.

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

How Nevada's first-in-nation earned wage access law works and why other states copied its licensing template.

Read article

Is earned wage access legal in Texas? How the state treats these apps, the bills that failed, and what it means for users.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking