May 2, 2026

Nevada Earned Wage Access Law and Its Impact

How Nevada's first-in-nation earned wage access law works and why other states copied its licensing template.

Read article

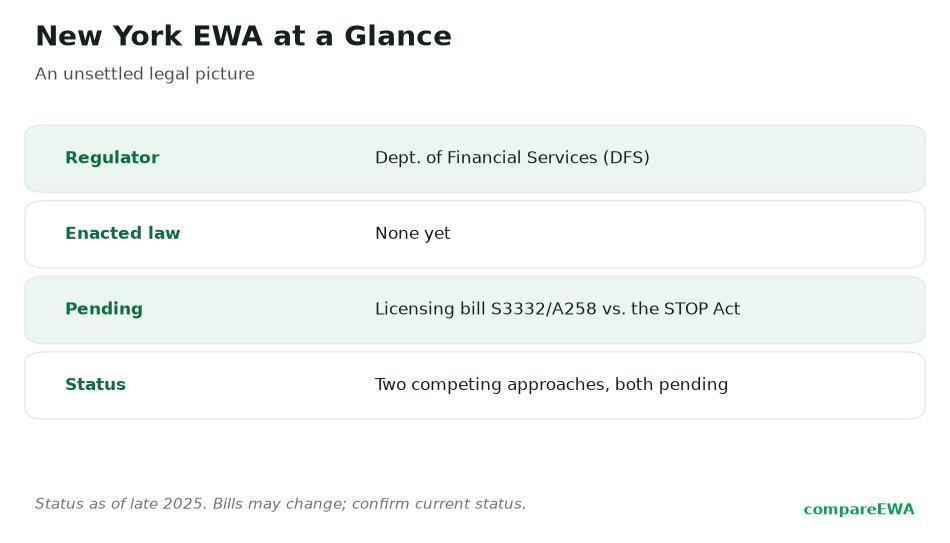

The New York earned wage access law is, right now, a question with two possible answers, and the state hasn't picked one. New York has no enacted EWA statute. What it does have is a pair of live bills pushing the product in opposite directions: one would license these apps as their own regulated category, the other would treat any wage advance as a loan and drop it under New York's famously strict usury cap. Which path wins will shape what a New York worker can be charged, and whether some of these apps can operate in the state at all.

Because nothing is settled, this piece is about where the rules stand, not where they've landed. Let me lay out both forks and what an unsettled picture means for you today.

For now, yes, cash advance apps operate in New York, and there's no New York-specific EWA licensing framework in force. The product isn't banned. But "no framework in force" is the key phrase, because two competing proposals are working through the 2025-2026 legislative session, and they'd produce very different outcomes for you.

Treat everything below as pending. I'm describing bills, not law. Bill status in New York can move quickly, and until one is signed, the current reality is simply that these apps run without a dedicated state rulebook.

New York is a high-stakes state for this debate for one reason above all: its usury law. New York enforces a 16% civil usury cap and a 25% criminal usury threshold. Those limits are low compared with most states, and they turn the abstract question "is EWA a loan?" into something with teeth. If a New York court or statute decides a fee-charging advance is a loan, that 16% ceiling suddenly becomes the measuring stick, and many app fee structures don't fit under it.

That tension is exactly why lawmakers have introduced two clashing bills instead of one tidy plan. One camp wants to carve EWA out as its own product with tailored rules. The other wants to fold it into existing lending law. They can't both become the New York earned wage access law, and the choice between them is genuinely live.

The first path is a licensing bill, S3332 in the Senate (with an Assembly companion, A258), sponsored by Senator Jeremy Cooney. It would require non-exempt EWA providers to get a license from the New York Department of Financial Services (the DFS) before operating in the state. As of the 2025-2026 session, S3332 was referred to the Senate Banks Committee on January 7, 2026. You can track it on the New York State Senate's S3332 page, and the Assembly companion at A258.

In its amended form, the bill sets out concrete consumer protections. Among them:

If this version becomes law, it would be one of the more protective EWA frameworks in the country, pairing hard fee caps with a mandatory free option and no credit reporting. That's a meaningfully better deal for a user than the uncapped approach some other states took. For contrast, our look at the California earned wage access law shows a state that regulated the product but declined to cap fees at all.

The competing path is the "STOP Act," introduced by Senator Samra Brouk and Assemblymember Steven Raga. Rather than create a new EWA category, it would deem any wage or cash advance a loan subject to New York's 16% civil usury cap. That's a far stricter approach, and it would reshape the market.

Here's why that's such a different world. If every advance is a loan capped at 16%, the fee-and-tip models that many apps rely on would run headlong into the usury ceiling. Some providers could not operate profitably under that math and might limit or withdraw their products in New York, the same dynamic that briefly played out in Connecticut when that state routed EWA through its Small Loan Act. Our piece on how Connecticut treats EWA like a loan shows what that classification did to app availability there.

Neither camp is obviously "right." The licensing bill accepts the product and tries to make it safer and cheaper. The STOP Act treats it as lending that should live under the same cap as other credit. They're two honest answers to the same question, and New York hasn't chosen.

In most states, arguing about whether EWA is "a loan" is a definitional exercise with modest consequences. In New York it's not, because of that 16% civil cap and 25% criminal threshold. The label doesn't just change paperwork here; it can determine whether a fee structure is even legal.

That's the through-line to keep in mind. New York's strict usury regime is the reason a licensing bill and a "treat it as a loan" bill lead to such different places. In a state with a 36% cap, an app might survive a "loan" classification. Under a 16% cap, many can't. So the stakes of the New York earned wage access law are unusually high compared with the average state.

Practically, a few things follow from all this uncertainty.

First, don't assume New York protections that don't yet exist. The fee caps, the mandatory free option, the no-credit-reporting rule: those live in a bill that hasn't passed. Until S3332 or something like it is signed, you can't count on them. Read each app's own terms rather than assuming a state floor.

Second, the federal backstop thinned out at the end of 2025. On December 23, 2025, the Consumer Financial Protection Bureau reaffirmed that qualifying earned wage access is not credit under the federal Truth in Lending Act and rescinded a July 2024 proposal that would have treated many of these products as credit. With the federal regulator stepping back, the direct-to-consumer question lands squarely on states like New York, which sharpens why this legislative fight matters. You can review the DFS's role and consumer resources at the New York Department of Financial Services, and read the statutory basis for the state's civil usury limit at General Obligations Law section 5-501.

Third, shop on cost, because nothing forces prices down in New York yet. Comparing instant-transfer fees, subscription charges, and tip defaults across apps is the only reliable protection you have while the law is unsettled. Our EWA app rankings put those numbers side by side, and if you're new to how these apps actually pull data from your account, start with whether cash advance apps are safe before you link anything.

One last caution: bill status changes fast, and committee action can shift the framing overnight. Check the New York State Senate and Assembly records for S3332, A258, and the STOP Act before relying on anything here, and phrase your own expectations as "pending," because that's genuinely what these rules are.

Yes, for now. Cash advance apps operate in New York, and there is no enacted New York-specific EWA licensing law in force. Two competing bills could change that, but neither has become law.

Not with a dedicated statute yet. New York has pending legislation, including a Department of Financial Services licensing bill (S3332 / A258) and the competing STOP Act, but the state has not enacted EWA-specific rules.

That is exactly the unsettled question. The STOP Act would treat any advance as a loan subject to New York's 16% civil usury cap, while the DFS licensing bill would regulate EWA as its own product. Until one passes, the classification is not fixed.

It is a proposed licensing framework sponsored by Senator Jeremy Cooney that would require non-exempt EWA providers to hold a DFS license. It includes fee caps of $5 for advances of $75 or less and $7 above that, a required no-cost option, and non-recourse terms. It was referred to the Senate Banks Committee on January 7, 2026.

Under the S3332 licensing bill, a provider could charge no more than $5 for a transaction of $75 or less and no more than $7 for a larger transaction, with voluntary tips excluded from the cap. Those caps would only apply if the bill becomes law.

It could, depending on which bill prevails. New York's 16% civil usury cap and 25% criminal threshold are why treating EWA as a loan would be so consequential here. Whether that cap applies to these apps is the central question the pending bills would resolve.

How Nevada's first-in-nation earned wage access law works and why other states copied its licensing template.

Read article

Is earned wage access legal in Texas? How the state treats these apps, the bills that failed, and what it means for users.

Read article

How California's DFPI treats earned wage access, what registration means, and what the rules change for you as a borrower.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking