June 26, 2026

Earned Wage Access Fees: What They Really Cost

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

When you search for an instant cash advance app, you are not shopping around. You need money now, tonight probably, and you want the app that delivers fastest. Fair enough. I will give you the fast options in a minute. But "instant" is not a feature these apps include for free. It is a paid upgrade, and the whole business is built on people reaching for it. Before you tap the fast button, it is worth turning that word into a real dollar figure so you know what the speed is actually costing you.

Here are the fastest-funding apps, their instant fees, and a straight answer on when paying for speed is smart and when it is money down the drain.

Every cash advance app has two speeds, and this is the thing to internalize first.

The standard transfer is free. It moves over the normal ACH bank rails and takes one to three business days. The instant transfer pushes the money to your debit card, usually within minutes, and you pay a fee for it. When an app calls itself "instant," it means the paid express option exists, not that fast money is the free default. Instant is the upgrade, standard is the base model, and the fee is the gap between them.

This matters because the express fee is not a side charge, it is the product. The CFPB's July 2024 study of the paycheck advance market found that expedited-delivery fees made up 96.6% of consumer-paid fee revenue by dollar value. The advance is close to a loss leader. Speed is what people actually pay for, and it is where nearly all of your cost hides.

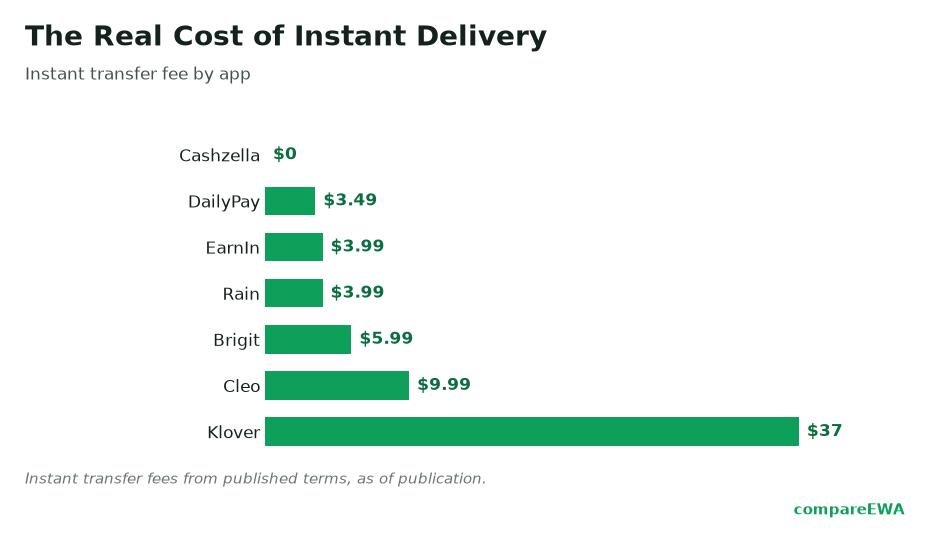

Here is a plain rundown of instant fees across the well-known apps. Treat these as figures to verify on each app's live page, because express fees change often and vary by state and by where the money is going (your own app account versus an external debit card).

Two things jump out of that list. First, the flat-fee apps (a few dollars regardless of amount) and the scaling-fee apps (fee grows with the advance) reward different sizes of advance. Second, Dave's structure quietly shows the escape hatch: keep the money inside the provider's own ecosystem and the express fee can vanish.

Do not read the sticker price. Read the ratio.

A $4 express fee sounds the same no matter what, but it is not the same. Pay $4 to move a $40 advance and you just paid 10% to get your own money a couple of days early. Pay that same $4 on a $200 advance and it is 2%, which is far easier to stomach. The dollar figure is identical; the deal is completely different.

So before you tap confirm, do one piece of mental math: divide the express fee by the advance amount. If the fee is a small slice of a meaningful advance, fine. If the fee is a fat percentage of a tiny advance, you are paying a steep premium for speed on money that was not much money to begin with. This one habit will save you more than any app choice, because it stops you from paying $4 to rush $40 you could have waited two days for.

Sometimes speed is the whole point. Your rent auto-drafts at midnight and the account is $60 short, or a utility is about to shut off, or the tow truck driver takes card and you have nothing on it. In those moments, a few dollars to make the money appear in ten minutes is a reasonable trade. The fee buys you out of a much larger problem.

Plenty of times, though, instant is a waste. If your payday is two days out and the bill is not due for four, a free standard transfer very likely arrives in time on its own. Paying $4 for instant there buys you nothing except the feeling of having acted. The honest gut-check is a single question: can this genuinely not wait one to three business days? If it can wait, take the free transfer and keep your money. If it truly cannot, pay for instant without guilt. Just make that an actual decision instead of a reflex.

Here is the outcome that quietly undoes the whole exercise. You pay $4 to get $100 instantly tonight. Payday comes, the app auto-debits its $104, and your paycheck is a little light or another bill cleared first. The account goes negative, and your bank charges an overdraft fee, often around $35.

Run that math and it stings. You spent $4 to rush the money, then $35 because rushing it left your account short on payday. The $4 was never the real risk. The real risk was borrowing right up against a paycheck that could not comfortably absorb the repayment. Getting money instantly and repaying on a tight payday is exactly the setup that triggers this, so leave yourself a cushion, and only borrow what next week's check can clearly cover.

If speed matters but you would rather not overpay for it, a few moves stack in your favor:

One more honest note on cost framing. A separate suit by the District of Columbia against EarnIn alleged that once instant fees and tips were counted, the effective APR on its advances topped 300%. That is an allegation from a state complaint, not a proven finding, so weigh it as a claim. But it points at the same reality this whole article is about: because the CFPB's December 2025 advisory opinion reaffirmed that optional expedite fees on qualifying earned wage access are not finance charges, no app has to show you an APR on the instant upgrade. Nobody prices the speed for you. You have to do it yourself, one advance at a time.

Several apps deliver instant transfers within minutes when you pay the express fee, including EarnIn's Lightning Speed and Brigit's instant option (roughly 20 minutes). Actual speed depends on your bank and debit card, and the "instant" option always costs more than the free one-to-three-day standard transfer.

Usually a few dollars, though it varies by app, amount, state, and destination. Common ranges run from under a dollar to around $15, and some apps (like Varo) scale the fee up with larger advances. The CFPB found the average expedited fee was about $3.18 per transaction.

Only when the money genuinely cannot wait one to three business days. If your bill is due before your free standard transfer would arrive, the fee is reasonable. If payday or the free transfer beats the deadline anyway, paying for instant buys you nothing. Divide the fee by the advance amount to judge whether the premium is fair.

Generally yes. Most cash advance apps do not run a hard credit check; they base your eligibility and limit on your bank activity and direct deposits instead. The instant part still costs an express fee, but qualifying usually does not depend on your credit score.

Because the express fee, not interest, is how these apps make most of their money. The CFPB found expedited-delivery fees made up 96.6% of consumer-paid fee revenue. The advance itself is nearly free to you; the speed is the paid product.

Use the free standard transfer and request it as early as possible, since it takes one to three business days. If your deadline is a few days out, the free transfer often arrives in time. Some apps also waive the instant fee when the money stays inside their own linked account rather than going to an external debit card.

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

Which cash advance apps offer the highest limits, how to qualify for more, and why the advertised max rarely matches your first advance.

Read article

A simple framework for choosing a cash advance app: line up limits, real cost, speed, and eligibility on the same criteria.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking