May 21, 2026

New York Earned Wage Access Law: The Rules Now

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

Most states that have tackled earned wage access built a brand-new category for it. Connecticut did the opposite. The Connecticut earned wage access law folds these advances into the state's Small Loan Act and, in plain terms, treats them as lending. That single decision, "this is a loan here," changes almost everything for a Connecticut user: whether your app is even available, what it can legally charge you, and what happens if you don't pay it back.

Connecticut also has the most interesting recent history of any state on this issue, because it went from effectively freezing the product out to writing a tailored licensing law in the span of about two years. Let me walk you through how that happened and what it means before you sign up.

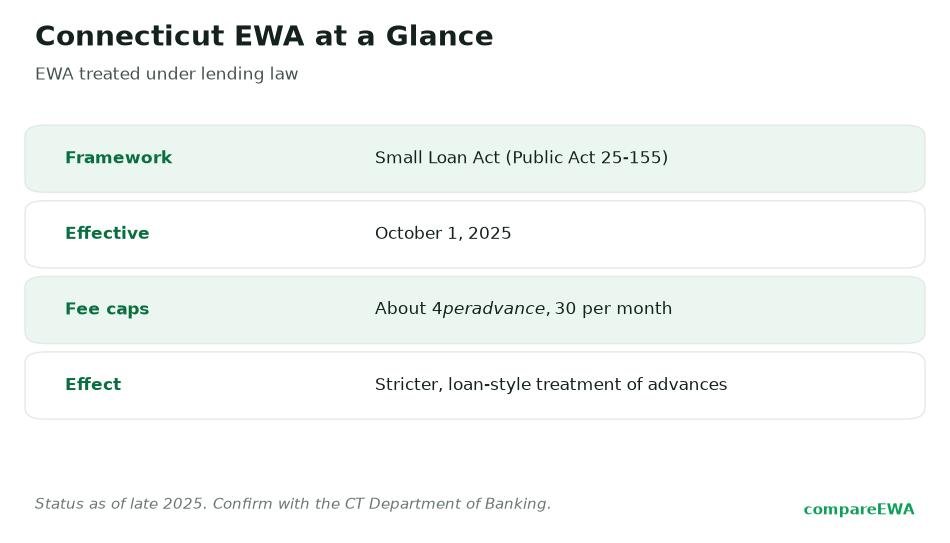

In Connecticut, an earned wage advance is legally a small loan. Public Act 25-155, which came out of Senate Bill 1396, was signed by Governor Ned Lamont on July 8, 2025, and took effect on October 1, 2025. It defines an EWA advance as a small loan, requires providers to be licensed under the Connecticut Small Loan Act, and caps what they can charge.

That framing is the whole story. In Nevada or California, the law says EWA is not a loan. In Connecticut, the law says it is. Everything else, the fee caps, the license, the protections, flows from that starting point.

Connecticut's position didn't appear overnight. It moved in stages.

In September 2023, the Connecticut Department of Banking issued guidance concluding that many EWA products already fell under the state's Small Loan Act. That wasn't a new statute, it was the regulator saying the existing lending law reached these products. The effect was immediate and blunt, and I'll explain it next.

Then, on July 8, 2025, Governor Lamont signed SB 1396 as Public Act 25-155, replacing that awkward guidance-based situation with a tailored licensing regime effective October 1, 2025. So the arc runs from "our existing loan law covers this" (2023) to "here's a purpose-built loan framework for it" (2025). The Connecticut Department of Banking remains the licensing and enforcement body throughout, and you can reach its license lookup and complaint tools at the Connecticut Department of Banking.

Here's the part that hit users directly. The Connecticut Small Loan Act carries a 36% APR usury cap. Once the 2023 guidance pulled EWA under that Act, most fee-charging providers couldn't make the math work. On the short repayment terms these advances use, a few dollars of fees translate into an APR-equivalent well above 36%, so operating profitably inside the cap was effectively impossible.

The result, through much of 2024, was that a number of apps paused or pulled out of Connecticut. If you were a Connecticut user who suddenly got a "not available in your state" message during that stretch, this is almost certainly why. The state hadn't banned the apps outright; it had priced the fee-based model out by treating it as regulated lending. That's a striking real-world example of what the "is it a loan?" question can do. For the broader picture of how these products stack up against traditional short-term credit, our comparison of earned wage access versus payday loans puts the cost side by side.

Public Act 25-155 gave providers a workable path back into Connecticut, but a tightly capped one. Here's what the law actually allows and requires:

Those caps are strict. A $4-per-advance or $30-per-month ceiling is far lower than what apps can charge in an uncapped state. For a Connecticut user, that's genuinely good news on cost, and it's the trade-off of the "it's a loan" approach: you lose some app availability, you gain a hard price limit. The legal detail here comes from analysis by firms tracking the change, including Goodwin's alert on Connecticut's EWA law, and trade coverage in American Banker's reporting on the Connecticut and Louisiana laws.

One nuance worth flagging honestly: classification can turn on the exact product design. FlexWage, an employer-integrated provider, published that Connecticut concluded its specific no-fee model was not treated as a loan. You can read the provider's own account of the FlexWage determination, but treat it as an interested party describing one narrow model. It likely applies to a specific no-fee, employer-integrated design, not to the fee-charging, direct-to-app products most consumers use. It's a nuance, not a blanket exemption.

Beyond the fee caps, the 2025 law carries the non-recourse protections that have become standard in state EWA laws. In Connecticut, a licensed provider cannot:

So even though Connecticut calls the advance a loan, it's a loan you can't be sued over, sent to collections on, or have reported to the credit bureaus for missing. That combination, "legally a loan, but non-recourse," is unusual, and it's worth understanding before you assume a "loan" label means the worst-case consequences. If you're weighing the safety of linking an app to your account in the first place, our guide to whether cash advance apps are safe covers what these apps can see and do once connected.

Connecticut's "it's a loan" stance runs directly against where the federal government landed. On December 23, 2025, the Consumer Financial Protection Bureau reaffirmed that qualifying "Covered EWA" products are not credit under the federal Truth in Lending Act, rescinding a July 2024 proposal that would have treated many of them as credit.

So you have a genuine split: the federal regulator declined to treat EWA as credit, while Connecticut regulates it as lending at the state level. That's not a contradiction you need to resolve, it's just the current reality. Because the federal rules don't attach in the way they would to traditional credit, the protection you actually rely on in Connecticut is the state law, not a federal one. The federal retreat is part of why state choices like Connecticut's carry so much weight now. This policy shift was widely anticipated; McGuireWoods flagged Connecticut and Louisiana as states poised to enact EWA legislation ahead of the signings.

A few practical takeaways for a Connecticut user. First, expect fewer apps but firmer limits. Not every provider that operates nationally will be licensed in Connecticut, and the ones that are can't charge more than $4 per advance or $30 per month. That's a cleaner deal on cost than you'll find in an uncapped state, even if the menu is shorter.

Second, don't take an app's word for its Connecticut status. Provider availability shifts, and licensing lists change. Confirm a provider is actually licensed through the Connecticut Department of Banking before you rely on it, rather than assuming an app is compliant just because it appears in your app store. Comparing the licensed options on cost and features still pays off, and our EWA app rankings and the way other states handled the same product, like the California earned wage access law, give you useful context for what a fair deal looks like.

Third, remember the trade-off you're accepting. Connecticut chose strong price protection over wide availability. Whether that's the right deal depends on how you'd use these apps, but at least in Connecticut you know the ceiling.

Yes, but it is regulated as lending. Public Act 25-155, effective October 1, 2025, defines an EWA advance as a small loan and requires providers to be licensed under the Connecticut Small Loan Act. Licensed apps can operate; unlicensed ones should not.

Finance charges are capped at no more than $4 per advance or $30 per month under the 2025 law. Providers must also offer at least one no-cost option per transaction and disclose how to choose it.

In September 2023 the Connecticut Department of Banking concluded many EWA products fell under the Small Loan Act, which carries a 36% APR cap. Most fee-charging providers could not operate profitably under that cap, so they paused or left the state until the tailored 2025 law took effect.

No. Under Public Act 25-155, a licensed provider cannot sue you for nonpayment, use third-party debt collectors, make unsolicited collection calls, or report nonpayment to the credit bureaus, even though the advance is legally treated as a loan.

Yes. The 2025 law requires at least one no-cost option per transaction, and the provider must disclose how you can choose it. You can pay for faster delivery, but you cannot be forced to pay to access your earned wages.

No. As of December 23, 2025, the CFPB reaffirmed that qualifying "Covered EWA" products are not credit under the federal Truth in Lending Act. Connecticut regulates EWA as lending at the state level despite that federal position, which is why the state law is what protects you here.

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

How Nevada's first-in-nation earned wage access law works and why other states copied its licensing template.

Read article

Is earned wage access legal in Texas? How the state treats these apps, the bills that failed, and what it means for users.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking