June 19, 2026

How to Stop Relying on Cash Advance Apps

A practical plan to treat cash advance apps as a bridge, not a habit, and shrink the advance you need each payday to zero.

Read article

You are hovering over the sign-up button, and part of you feels a little embarrassed for even being here. Let me say this first, before anything else: needing a few dollars a week early is a timing problem, not a character flaw. Rent does not care that your paycheck lands on Friday and the auto-draft hits Wednesday. That gap is real, and wanting to close it does not make you bad with money.

So let us skip the sales pitch and the scare stories. This is a plain, honest self-check to help you figure out whether an earned wage access (EWA) app actually solves your problem, or just slides the shortfall forward a week. By the end you should know which one it is for you, without anyone wagging a finger.

If money feels tight right up against payday, you have plenty of company. The Federal Reserve runs a big annual survey on how households are doing, and in its 2024 report only 63% of adults said they could cover a hypothetical $400 emergency entirely with cash or its equivalent. That means roughly one in three could not. It is down from a high of 68% in 2021.

Look a little lower on the ladder and it gets thinner. In that same survey, 18% of adults said the largest emergency expense they could handle from savings alone was under $100. Under a hundred dollars. So if a surprise car repair or a shifted due date would put you in a bind, you are squarely in the middle of the pack, not off in some corner by yourself.

The FDIC found something similar from another angle: about 14.2% of U.S. households in 2023 were underbanked, meaning they used nonbank financial products to make ends meet. Tools like EWA exist because a lot of regular, working people hit the same wall. Knowing that will not pay your bills, but it should take the shame out of the decision. Deciding clearly is easier when you are not also fighting embarrassment.

An advance shines in one specific situation: a genuine, one-time timing mismatch. Your paycheck lands Friday. Your rent auto-drafts Wednesday. You are not short on the month, you are short for two days. Pulling $80 to bridge that gap can save you a $35 overdraft fee or a late charge that costs far more than the advance did.

That is the honest, useful version of these apps. When the fee you pay is smaller than the fee you avoid, and the gap does not come back next week, the math works in your favor. Think of it like a bridge over a puddle. You cross once, and you are on dry ground on the other side.

The trouble starts when it is not a puddle. It is the tide.

Here is the question that matters more than any other: is this a one-time gap, or does the same gap reopen every single pay period?

When you pull $100 today, next week's paycheck arrives $100 (plus any fee) shorter. If your budget was already stretched, that smaller paycheck leaves you short again, so you advance again. And again. The advance did not close the gap. It just moved it forward and took a small toll each time it crossed.

The data shows this is a real pattern, not a scare tactic. The CFPB found that people using these apps took an average of about 27 advances per year. California's financial regulator, the DFPI, studied direct-to-consumer apps in its state and found users averaged around 36 advances a year, with some hitting 100. That is not a once-in-a-while bridge. That is a standing part of the monthly cash flow.

None of that means you did something wrong. It means the tool is treating a symptom (this week is short) instead of the cause (every week is short). If you can spot which situation you are in, you have already made the hard part of this decision.

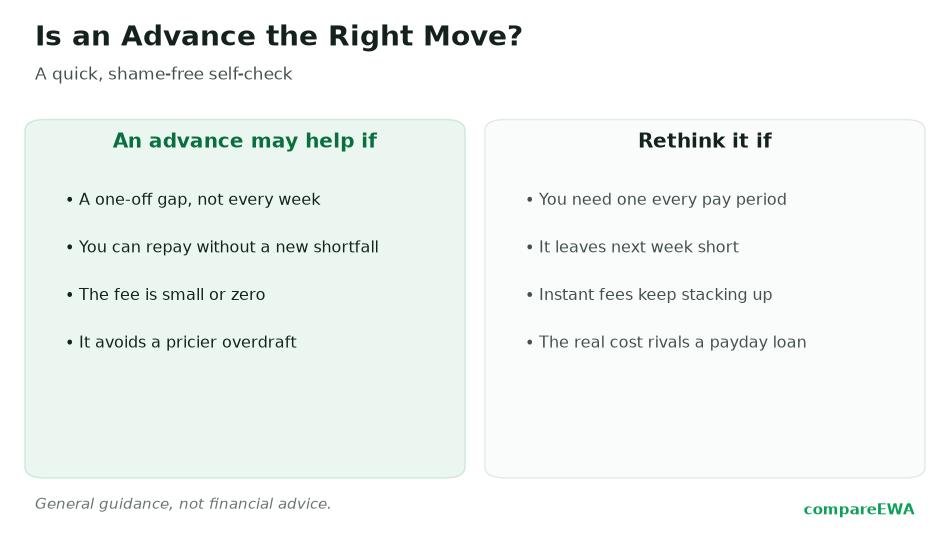

Sit with these five questions before you tap anything. Answer them like you would for a friend, not like you are trying to pass a test.

If you answered "one-time," "no loop," "cheaper than the alternative," and "true need," an advance is probably a reasonable call this once. If you kept landing on "repeating" and "loop," the app is not really the answer, and I will get to what is.

Let me make this concrete, because the dollars look tiny until they do not. Say you advance $100 and pay a $5 express fee to get it instantly.

Used once: You paid $5 to avoid, let us say, a $35 overdraft. You are $30 ahead. Clean win. Cross the puddle, move on.

Used every payday, twice a month: That is 24 advances a year at $5 each, so $120 in fees over twelve months for the privilege of staying exactly where you started. And that is before tips. Some apps nudge you toward an optional "tip" on top. California's regulator added up all the fees and tips on the advances it studied and found the effective annual rate landed around 331% to 334%. That figure counts optional tips and is debated, so take it as a ceiling rather than a fixed price. Still, it makes the point: a $5 charge that repeats behaves a lot more like expensive credit than like a small convenience fee.

The single advance and the every-paycheck habit start from the same $5. They end up in very different places. That is the whole decision in one picture.

If you like a quick gut-check, here is how I would sort it.

Green light (an advance probably helps): a rare timing gap, a fee smaller than the overdraft or late charge you are dodging, and a next paycheck that still covers your bills after the advance comes out.

Yellow light (proceed carefully): you have used it two or three times recently, you are eyeing the paid instant transfer when you could wait for the free one, or you are not totally sure next week will be fine. Use it if you must, but pair it with one small fix so it does not become a habit.

Red light (the app is masking a bigger gap): you advance nearly every payday, your paycheck is spoken for before it lands, or you are tipping and paying express fees on money you then need to re-borrow next week. This is not a willpower failure. It is a signal that the shortfall is structural, and an advance cannot patch a structural hole.

Landing on red or yellow is not a dead end. It is useful information, and there are calmer moves than one more advance.

Start by shrinking the gap instead of feeding it. Call one biller and ask to move a due date to just after payday. Many utilities and lenders will do it for free, and it can erase the mismatch that sent you to the app in the first place. Pick one recurring cost you would not miss and trim it, then send that same small amount toward a tiny starter cushion. Even a few hundred dollars set aside quietly ends the loop, because it covers the exact timing gap the app was covering, without the fee.

And if you do use an advance while you build that cushion, use it as a bridge with a plan on the other side, not as the plan itself. There is no shame in either choice. The only move worth avoiding is paying to stand still without noticing you are doing it.

No. Using one is not a moral failing. It is a cash-flow tool. It becomes a problem only when you rely on it every pay period to cover a shortfall that never closes, because then you are paying fees to stay in the same spot. A one-time bridge to avoid a bigger fee can be a smart call.

Ask whether your gap is a one-time timing issue or a repeating one. If your paycheck runs short at the same point every cycle, an advance treats the symptom, not the cause. If it is a rare mismatch and the fee is smaller than the overdraft or late charge you would otherwise pay, it can genuinely help.

There is no official line, but a good rule of thumb: if you need an advance most pay periods, that is too often. At that point you are borrowing from next week to pay for this week, and studies show frequent users average dozens of advances a year. Treat repeated use as a sign to close the underlying gap instead.

Once, no. A $4 or $5 fee to avoid a $35 overdraft is a fine trade. Repeated, yes. The same small fee charged 24 times a year is over $100, and when you add optional tips the effective annual rate can climb into the triple digits. The problem is not the single fee, it is the repetition.

Try the free moves first: ask a biller to shift a due date to just after payday, split one large bill into two smaller paycheck-aligned payments, or trim one recurring cost. Then route that freed-up money into a small starter buffer of a few hundred dollars, which covers the same timing gap the app was covering, without the fee.

Most EWA apps do not run a hard credit check and do not report your advances to the major credit bureaus, so a single advance typically will not raise or lower your score. Terms vary by provider, so read the specific app's disclosures rather than assuming. If you are worried about credit impact, that is a good reason to check before you sign up.

A practical plan to treat cash advance apps as a bridge, not a habit, and shrink the advance you need each payday to zero.

Read article

How to build an emergency fund on a low income, with realistic weekly amounts and habits that make a starter buffer stick.

Read article

Small, doable moves to make your paycheck last through the long last week before payday, built on realistic numbers.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking