May 10, 2026

Does My Employer Offer Daily Pay? How to Check

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

It's 9 p.m. on a Tuesday. You've been driving since noon, the app says you cleared a decent day, and rent is due tomorrow. The problem is simple and maddening: the money you earned is sitting somewhere between the platform and your bank, not in the account the landlord's autopay will hit at 6 a.m. You did the work. The cash just isn't where it needs to be yet.

That gap is exactly what instant pay exists to close. If you drive for Uber or Lyft, deliver for DoorDash or Instacart, or run routes for Amazon Flex or Spark, you've probably seen a "cash out" button that promises money in minutes. This article is about what that button actually does, what each platform charges as of publication, and the one move most drivers skip that would save them the fee entirely. It's written for gig workers using platform cash-out features, and it also covers third-party cash advance apps as a separate option, because those two things get lumped together and they are not the same.

Regular payroll runs on a schedule. A traditional employee gets paid every two weeks whether they need the money Tuesday or not. Gig work flipped that. Because you're an independent contractor, the platform tracks what you make trip by trip, and instant pay lets you move that balance to a debit card on demand instead of waiting for the weekly deposit.

Here's the part worth understanding before you tap anything: platform instant pay is not a loan. It is not an advance against money you haven't made yet. It's early access to earnings that already belong to you, including tips in most cases. Nobody is fronting you anything. That distinction matters because it changes the cost math and the risk. A loan can trap you. Moving your own money faster can't, at least not in the same way, though the fees still add up if you're careless about them.

The mechanics are consistent across the big platforms. You link an eligible debit card, the app shows your available balance, you request a transfer, and the money usually lands in minutes. "Usually" is doing some work in that sentence, and we'll get to why.

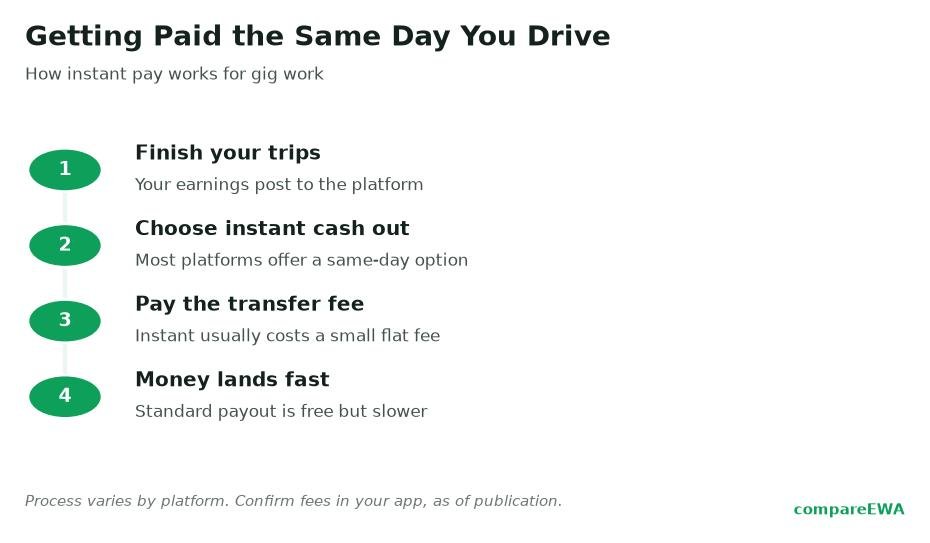

Once you finish trips, your earnings pile up in the driver app as an available balance. Instant pay lets you sweep that balance to your linked debit card any time, up to a daily limit and a maximum number of cash-outs per day. Most platforms require a small minimum balance before you can pull, which is the thing that trips people up when they've only done one short trip and the button won't work yet.

The transfer itself runs over the debit card networks, which is why it's fast, and it's also why it sometimes isn't. When everything's healthy, money shows up in a minute or two. When your bank flags it, or the card network is slow, or it's a weekend, that "instant" transfer can sit for a business day or more. If you're timing a cash-out against a bill that clears at dawn, build in a cushion. Don't cash out at 11:58 p.m. and assume it'll beat a midnight autopay.

Fees change constantly and vary by city, so treat every number here as a snapshot and check the platform's own help page before you rely on it. As of publication, here's the lay of the land.

Uber Instant Pay charges about $1.25 per cash-out when you use a personal debit card, and you can cash out up to six times a day. Lyft Express Pay runs roughly $1.75 per transfer, with a cap of about five transfers per 24 hours and a minimum earnings threshold before you can pull. DoorDash Fast Pay is around $1.99 per withdrawal. Some cities have their own rules layered on top; Uber in New York, for example, has operated under different cash-out terms than the rest of the country. That's the whole reason to confirm your fee in your city rather than trusting a number you read somewhere.

Look at those figures next to each other and a pattern jumps out. A buck twenty-five here, a couple dollars there, it feels like nothing in the moment. It is not nothing when you do it every single day.

Here's the thing the veteran drivers know and the new ones learn the expensive way: each major platform offers its own banking card that waives the per-transfer fee. Uber has the Uber Pro Card, which can pay you automatically after every trip with no per-transfer charge. Lyft has Lyft Direct. DoorDash moved its fee-free instant payouts to its Crimson banking account after DasherDirect shut down on April 1, 2025.

Switch your payouts to the platform's own card and that daily $1.99 problem mostly disappears. You get your money fast, or in Uber's case automatically after each trip, and you stop leaking cash on transfer fees. For anyone cashing out daily, this is the single biggest money-saver available, and it costs nothing to set up.

There's a tradeoff worth naming. These cards are separate accounts, so you may have to move money to your regular bank if that's where your bills pull from, or switch your autopays over to the new card. That's a one-time hassle. Weigh it against paying a fee every day for the rest of your driving career and the math answers itself.

Let's put real numbers on it, because "small fee" hides the damage. Say you drive most days and cash out through DoorDash Fast Pay at $1.99 a pull. Do that six days a week and you're spending about $12 a week, roughly $52 a month, and a little over $620 a year. On Lyft at $1.75, daily cash-outs run close to $640 a year. On Uber's $1.25, you're looking at somewhere around $450 a year if you pull once a day.

Six hundred dollars is a set of tires. It's a couple weeks of groceries. It's money you earned and then handed back for the convenience of getting it a few days early, when the fee-free card would have gotten it to you just as fast. If cash flow forces you to cash out daily, fine, that's a real situation and there's no shame in it. Just do it on a card that doesn't charge you for the privilege.

One more option if you're stuck paying per-transfer fees for now: batch your cash-outs. Instead of pulling after every shift, pull once every two or three days when you can. You cut the number of fees roughly in half without changing what you actually earn.

People use "instant pay" and "cash advance app" like they mean the same thing. They don't, and the difference can cost you.

Platform instant pay moves money you've already earned. Third-party cash advance apps are a separate category: you download them on your own, link your bank account, and they estimate your income to front you a small amount before your next deposit. For a lot of gig workers these apps are appealing because your income is irregular and hard to advance against through a normal employer. But the cost structure is different. Many charge a subscription, an express-delivery fee to get the money fast, and prompt you for a "tip" that isn't really optional if you want a decent limit next time.

The federal picture on these apps shifted recently. A CFPB advisory opinion on December 23, 2025 reaffirmed that qualifying employer-partnered earned wage access is not treated as credit under the Truth in Lending Act, and the Bureau has favored models that offer a fee-free option and clearly disclose optional expedited-transfer costs. That framing applies to the earned wage access and advance-app category, not to platform instant pay, which is just early access to your own earnings. If you're weighing a third-party app, read what it charges in total, tips and express fees included, and compare that to simply using your platform's fee-free card.

Fast money has a quiet downside that has nothing to do with fees. When you cash out every day, you never see a week's earnings sitting together, so you never quite notice how thin they are after gas, tolls, and the wear you're putting on your car. The daily transfer feels like a win each time, and it papers over a slow week you'd otherwise catch.

Gig income is volatile even when your annual pay holds steady, which the JPMorgan Chase Institute has documented in its work on earnings instability. Some weeks are strong, some are lean, and the average is what actually pays your bills. So pair fast pay with a habit: once a week, add up what you brought in and subtract what the car cost you (gas, maintenance set-aside, the miles). Track the net, not the gross. The cash-out button tells you what's available. It doesn't tell you whether the week was any good. That's on you to know.

For context on how many people this touches, the BLS Contingent and Alternative Employment Arrangements data from July 2023 counted 11.9 million independent contractors, about 7.4 percent of employment, plus millions more in on-call and alternative arrangements. App-based gig work is almost certainly larger than the survey's "about 1 percent used apps to arrange work" figure suggests, since the methodology undercounts side and multiple-job hustles. Point being, you're far from alone in living on same-day money. The workers who come out ahead are the ones who get it fast and cheap and still keep an honest eye on the totals.

As of publication, Uber Instant Pay is about $1.25 per cash-out with a personal debit card (up to six per day), Lyft Express Pay is roughly $1.75 per transfer (about five per day), and DoorDash Fast Pay is around $1.99 per withdrawal. Fees change often and vary by city, so confirm the current amount on each platform's help page.

Use the platform's own banking card. The Uber Pro Card, Lyft Direct, and DoorDash Crimson waive the per-transfer fee, and Uber's card can pay you automatically after every trip. Switching to the fee-free card is the biggest saver for anyone who cashes out daily.

Usually within a minute or two, but it can take up to a few business days if your bank flags the transfer, the card network is slow, or it's a weekend. Don't cash out at the last second before a bill clears; leave yourself a cushion.

No. Platform instant pay is early access to money you already earned, including tips, so nothing is being fronted to you. A cash advance app is a separate product that fronts you money before payday and typically charges subscription, express, or tip costs.

Rarely, once you know a fee-free card exists. Paying about $1.99 a day works out to more than $600 a year for money you could move just as fast for nothing. If you're stuck on per-transfer fees, batch your cash-outs to cut how many you pay.

Several third-party apps estimate income from your bank deposits and advance a small amount to workers without a fixed paycheck. Read the total cost, including any subscription, express fee, and requested tip, and compare it to using your platform's fee-free card before you rely on one.

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

How same-day and on-demand pay reshapes cash flow for workers used to a biweekly cycle, and the tradeoffs of pulling pay early.

Read article

How earned wage access works for hourly and shift workers with variable hours, and what you can safely pull before payday.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking